How the Iran War Is Reshaping Industrial Buying

Supply chain disruption has returned, but it looks different this time.

During COVID-19, disruption was driven by shutdowns and demand shocks. Today, the pressure is coming from geopolitical instability, trade route risk, and cost volatility. While factories remain open, the system around them is becoming less predictable.

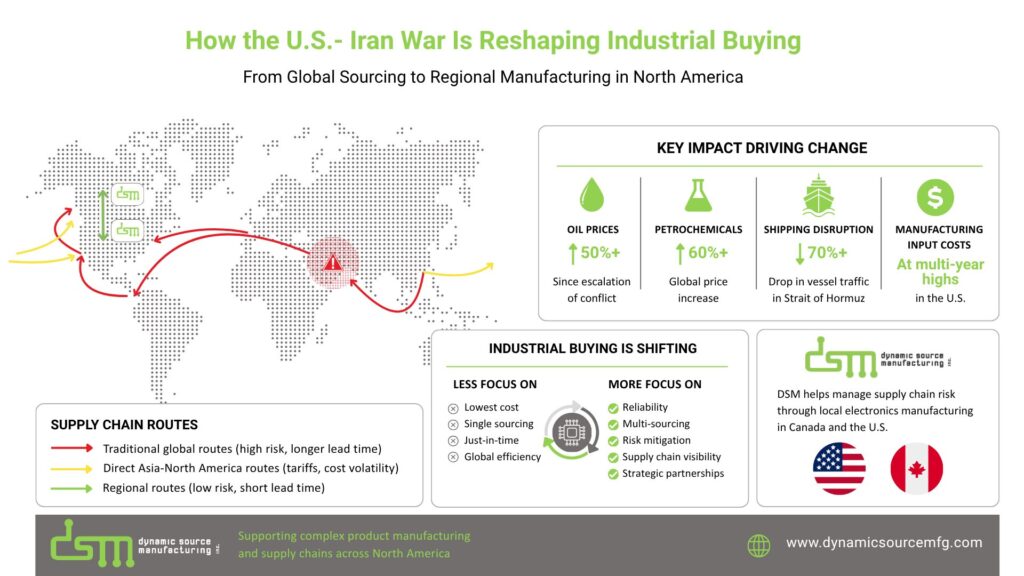

One of the clearest signals is maritime traffic through the Strait of Hormuz. Since the escalation of tensions, vessel traffic has dropped sharply, with some estimates pointing to declines of up to 70% in certain periods. At the same time, reports indicate that hundreds of vessels have faced delays or rerouting due to security concerns and insurance restrictions.

As a result, manufacturers are not dealing with stoppages. Instead, they are dealing with instability. Lead times fluctuate, freight costs shift weekly, and planning horizons are shrinking again. That environment is already influencing how procurement teams make decisions.

![]()

Cost pressure is the biggest driver of procurement change

Cost pressure has quickly become the most immediate and measurable impact of the conflict.

Energy markets reacted first. Oil prices rose by more than 50% during peak escalation periods, which then flowed directly into transportation, materials, and production costs. Petrochemical prices followed, with increases of over 60% in some segments. At the same time, U.S. manufacturing data shows input costs reaching their highest levels in several years.

Compared to COVID, the dynamic is different. In 2020–2021, cost increases were tied to shortages and demand spikes. Today, they are driven by structural factors such as energy, insurance, and logistics risk. Because of that, companies are less focused on finding the lowest-cost supplier and more focused on cost stability.

Procurement teams are adjusting accordingly. They are prioritizing predictability, contract security, and supplier proximity, even when nominal costs are higher.

Critical material shortages are re-emerging

Material availability is once again becoming a constraint, particularly for industries that depend on specialized inputs.

Helium is one example. It is essential for semiconductor manufacturing, aerospace systems, and fiber optics. Supply disruptions tied to the region have already created pressure in global markets, raising concerns about availability for high-tech production.

At the same time, petrochemical derivatives, which are used in plastics, coatings, and packaging, are becoming more expensive and less predictable. Given that plastics are involved in the majority of manufactured goods, the impact is broad.

Unlike during COVID, when shortages were driven by factory shutdowns, today’s constraints are tied to upstream inputs. That distinction matters. It means even well-functioning supply chains can become constrained if critical materials are delayed or repriced.

Canada and U.S. procurement are shifting in parallel

The impact is visible across North America, although it is playing out slightly differently in Canada and the United States.

In Canada, importers are already dealing with freight delays, rerouting, and capacity challenges. Logistics providers are adjusting routes to avoid high-risk regions, which adds time and cost to shipments. At the same time, rising energy prices are feeding directly into transportation and production costs across industries.

Governments and industry groups are also responding more proactively than in previous cycles. For example, regional task forces have been created to monitor supply chain risk and coordinate responses.

In the United States, manufacturing activity has remained relatively stable, but cost pressure and uncertainty are increasing. Companies are still producing, yet they are becoming more cautious in hiring and expansion decisions.

As a result, procurement strategies are evolving in both markets. There is a stronger emphasis on dual sourcing, supplier consolidation, and regional partnerships.

Diversification and regionalization are accelerating

The current conflict is reinforcing a shift that began during COVID but had not fully stabilized. Global supply chains are continuing to diversify. However, diversification no longer means simply adding more international suppliers. Increasingly, it includes bringing production closer to end markets.

Energy policy discussions also reflect this trend. Countries are rethinking dependency on critical regions and exploring more localized or allied supply networks. For manufacturers, this translates into a more regional approach. North America is becoming more strategically important, not just for political reasons, but for operational resilience.

Industrial buying is shifting toward risk management

All of these factors are changing how industrial buying decisions are made. Before COVID, procurement was largely driven by cost optimization. During COVID, availability became the primary concern. Today, the focus is shifting again, this time toward risk management.

Companies are asking different questions:

- How stable is this supplier over the next 12–24 months?

- How exposed is this supply chain to geopolitical disruption?

- How quickly can we adjust if conditions change?

As a result, procurement teams are becoming more conservative. They are building buffer inventory, reducing supplier churn, and strengthening relationships with trusted partners.

This approach may not minimize cost in the short term, but it reduces volatility and protects program execution.

Managing supply chain risk in a changing environment

In this environment, manufacturing strategy becomes part of supply chain strategy.

Working with partners that operate within North America can help reduce exposure to global disruptions. Proximity allows for faster iteration, better communication, and greater visibility into production. At the same time, it supports compliance with domestic procurement requirements and funding criteria.

At DSM, we work with OEMs across Canada and the U.S. to support programs that require consistency, flexibility, and control. Our manufacturing footprint is designed to help customers navigate exactly this kind of environment, where stability matters as much as cost.

![]()

The U.S.–Iran conflict is not creating an entirely new supply chain reality. Instead, it is accelerating changes that were already underway.

Companies that adapt their procurement strategies now, with a stronger focus on resilience and regional alignment, will be better positioned to manage uncertainty and maintain performance in the long term.

Reach out today: dsmsales@dynamicsourcemfg.com

Book a facility tour: Contact DSM

{kind=link}